• Three HRC lines were commissioned from January to August 2025, located in North China, South China, and Central China.

According to SMM statistics, three new HRC production lines were commissioned by domestic steel mills from January to August 2025, with a combined capacity of approximately 10.58 million mt. The newly commissioned lines are distributed across North China, South China, and Central China. Due to factors such as funding constraints, government approval delays, and adjustments in steel mills' strategic layouts, the overall commissioning progress of HRC capacity this year fell short of earlier expectations.

• Over 30 million mt of HRC capacity is expected to be commissioned, though some projects may be shelved.

As of August 29, the SMM survey compiled domestic steel mills' planned HRC production lines, indicating 13 additional lines with a cumulative capacity of 38.84 million mt. By region, North, Central, and Northwest China will add 11, 1, and 1 line(s), respectively. However, SMM notes that some lines remain pending, and certain projects may ultimately be shelved.

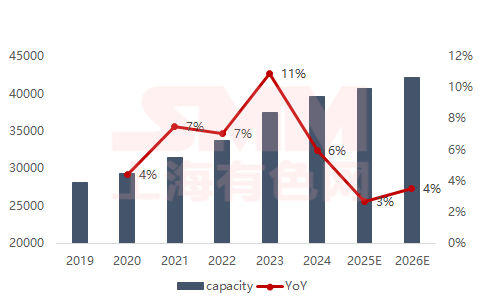

• HRC capacity growth peaked in 2023, slowing from 2024 to 2025.

SMM statistics show 10.58 million mt of new HRC capacity will be added in 2025. Excluding potential H2 commissioning, total national capacity is projected at 406.64 million mt, up 3% YoY from 2024, marking a clear slowdown compared to the 2023-2024 growth rate.